Supply and demand is a fundamental concept in economics that is crucial for understanding the workings of modern society. At its core, the theory of supply and demand is about the relationship between the quantity of a product or service that is available and the amount that people want to buy. This article aims to provide a comprehensive overview of supply and demand, including its basic principles, key terms, and practical applications.

The Basic Principles of Supply and Demand

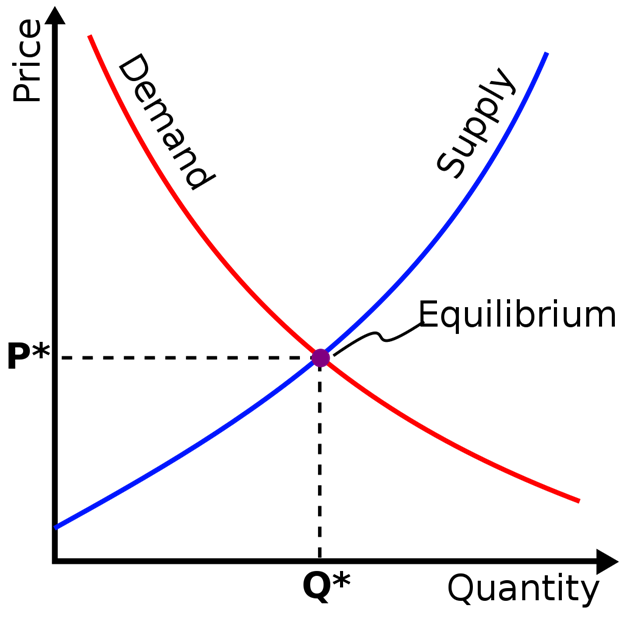

At its simplest, the theory of supply and demand is based on the idea that the price of a product or service is determined by the amount that people want to buy (demand) and the amount that is available (supply). When demand is high and supply is low, prices will typically rise, while when supply is high and demand is low, prices will fall. This relationship between supply and demand is often depicted graphically as a curve, with the intersection of the two curves representing the equilibrium price at which the quantity of goods supplied equals the quantity of goods demanded.

Key Terms and Concepts

Supply: The amount of a product or service that producers are willing and able to sell at a given price and time. Example: A bakery produces 100 loaves of bread per day at a price of $5 per loaf.

Demand: The amount of a product or service that consumers are willing and able to buy at a given price and time. Example: A consumer purchases two loaves of bread per week at a price of $4 per loaf.

Equilibrium: The point at which the quantity of a product or service demanded by consumers equals the quantity of the product or service supplied by producers, resulting in a stable market price. Example: The bakery produces 100 loaves of bread per day, and consumers purchase 100 loaves of bread per day at a price of $5 per loaf.

Surplus: A situation in which the quantity of a product or service supplied exceeds the quantity demanded, resulting in a lower market price. Example: The bakery produces 150 loaves of bread per day, but consumers only purchase 100 loaves of bread per day at a price of $4 per loaf.

Shortage: A situation in which the quantity of a product or service demanded exceeds the quantity supplied, resulting in a higher market price. Example: The bakery produces 50 loaves of bread per day, but consumers demand 100 loaves of bread per day at a price of $6 per loaf.

Elasticity: A measure of how sensitive consumers or producers are to changes in price or income. Example: If the price of bread increases from $5 to $6 per loaf, and consumers reduce their purchases from two loaves per week to one loaf per week, the price elasticity of demand for bread is 0.5.

Inelasticity: A measure of how insensitive consumers or producers are to changes in price or income. Example: If the price of insulin increases from $100 to $150 per vial, and consumers continue to purchase the same amount of insulin, the price elasticity of demand for insulin is less than 1, indicating inelasticity.

Substitute: A product or service that can be used in place of another product or service. Example: If the price of beef increases, consumers may purchase chicken as a substitute.

Complement: A product or service that is typically used together with another product or service. Example: If the price of gasoline increases, the demand for cars may decrease, as gasoline and cars are complements.

Market: A place or mechanism where buyers and sellers come together to trade products or services. Example: The stock market is a mechanism where buyers and sellers come together to trade stocks.

Another important concept is the law of diminishing marginal utility, which states that as a person consumes more of a good or service, the additional satisfaction they derive from each additional unit of the good or service decreases. This means that the more of a good or service a person has, the less willing they will be to pay a high price for additional units.

Practical Applications

Understanding supply and demand is not just a theoretical concept, but it has practical applications in our daily lives. One of the most common applications is pricing. Businesses use supply and demand to determine the price of goods and services. When demand for a product or service is high and supply is low, the price goes up. Conversely, when demand is low and supply is high, the price goes down. This is why the price of a product can fluctuate based on the time of year, current events, or even the weather. For example, during the holiday season, demand for toys increases, and the prices tend to go up.

Another practical application of supply and demand is in the job market. The labor market operates under the principles of supply and demand, just like any other market. When there is high demand for a particular job or skill set, salaries tend to increase. For instance, in recent years, there has been a growing demand for individuals with data science skills, and as a result, data scientists are among the highest-paid professionals in the market.

Furthermore, understanding supply and demand can help individuals make better financial decisions. For instance, when purchasing a home or investing in the stock market, knowledge of supply and demand can help individuals make informed decisions. If there is a limited supply of a desirable property, the price may be driven up, and if there is a high demand for a particular stock, the price may rise as well.

In the world of agriculture, supply and demand play a crucial role in determining the prices of crops. Farmers must consider factors such as weather patterns, consumer demand, and transportation costs to determine what to grow and how much to charge. A shortage of crops due to natural disasters or a sudden increase in demand for a specific crop can cause prices to skyrocket.

In conclusion, understanding supply and demand is essential for making informed decisions in various areas of life. Whether it’s pricing, the job market, investments, or agriculture, knowledge of supply and demand can provide valuable insights that can help individuals make better decisions. It’s a fundamental concept that has been studied by economists for centuries, and its applications continue to be relevant today.

Impacts of Technological Advancements

The world is experiencing a rapid advancement in technology, and the business world is no exception. Technology has led to significant changes in how businesses operate, and these changes have impacted various industries and job markets. In this section, we will explore some of the specific ways that technological advancements have affected the supply and demand of labor.

One of the most significant impacts of technological advancements is the displacement of workers in certain industries. For example, the rise of automation has led to the displacement of many manufacturing jobs, as robots and machines can perform tasks more efficiently and cost-effectively than humans. According to a report by the Brookings Institution, the use of robots and automation in manufacturing has led to a net loss of over 700,000 jobs in the United States alone between 1990 and 2007 (Beaudry, Green, & Sand, 2016). This trend is expected to continue in the coming years as technology continues to advance.

The impact of technological advancements is not limited to manufacturing jobs. Advancements in artificial intelligence (AI) and machine learning are also leading to significant changes in the demand for certain types of workers. For example, a report by the McKinsey Global Institute estimates that by 2030, up to 800 million jobs worldwide could be displaced by automation (Chui, Manyika, & Miremadi, 2017). However, the same report also suggests that technology will create new jobs, and the net impact on the job market will depend on the ability of workers to adapt to the changing technological landscape.

One industry that has been heavily impacted by technological advancements is the transportation industry. The rise of ride-sharing services like Uber and Lyft, as well as advancements in autonomous vehicle technology, has led to significant changes in the demand for certain types of workers. According to data from the Bureau of Labor Statistics, the number of taxi drivers and chauffeurs in the United States decreased by 20% between 2014 and 2019 (Bureau of Labor Statistics, 2020). While ride-sharing services have created new job opportunities for drivers, they have also led to increased competition and lower wages in the industry.

Another industry that has been heavily impacted by technological advancements is the retail industry. The rise of e-commerce has led to significant changes in the demand for workers in traditional brick-and-mortar retail stores. According to a report by the National Retail Federation, the number of retail workers in the United States decreased by over 500,000 between 2001 and 2016 (National Retail Federation, 2017). While e-commerce has created new job opportunities in areas like warehousing and logistics, it has also led to increased competition and lower wages in some industries.

In sum, technological advancements have had a significant impact on the supply and demand of labor across various industries. While these changes have led to the displacement of some workers, they have also created new job opportunities in other areas. The key to adapting to these changes is to stay informed about the latest technological advancements and to continually update one’s skills to meet the demands of the changing job market.

Criticisms of the Theory of Supply and Demand

While the theory of supply and demand is widely accepted among economists and business leaders, it is not without its critics. One common criticism is that the theory assumes perfect competition, which is often not the case in the real world. Perfect competition is a theoretical market structure in which no single buyer or seller can affect the price of a good or service. In other words, the market is characterized by many buyers and sellers, homogenous products, perfect information, and low barriers to entry and exit. While this may seem like an ideal market structure, it is problematic in practice. In fact, consumers and producers rarely have complete knowledge about the market, leading to market inefficiencies.

Additionally, perfect competition often results in a race to the bottom in terms of prices. Without any differentiation in products, companies are forced to compete solely on price, leading to lower profits and potentially lower quality products.

External factors also play a significant role in supply and demand. For example, weather patterns can affect the supply of agricultural goods, while geopolitical tensions can influence the price of oil. Additionally, government regulations can impact the market, such as environmental regulations on carbon emissions or minimum wage laws. These regulations can increase the cost of production, leading to higher prices for consumers.

Environmental factors are also becoming increasingly important in the market. As consumers become more aware of the impact of their purchasing decisions on the environment, they may demand more sustainable products or products that are produced in an environmentally-friendly manner. This can drive up the cost of production and affect the supply and demand for certain goods.

For instance, the recent surge in demand for electric cars has been influenced by both government regulations and consumer preference for more sustainable options. The increasing demand has resulted in increased production, which has in turn led to a reduction in production costs. As a result, electric cars are becoming more affordable for consumers. Similarly, the market for renewable energy has been influenced by government subsidies and regulations aimed at reducing carbon emissions.

In summary, while perfect competition may seem like an ideal market structure in theory, it is problematic in practice. External factors such as government regulations, environmental concerns, and technological advancements can have a significant impact on supply and demand, leading to market inefficiencies and challenges for businesses. Understanding these factors is critical for businesses looking to operate in a dynamic and ever-changing market.

Conclusion

Supply and demand is a critical concept that underpins many of the most important aspects of modern society, from the pricing of goods and services to the health of labor markets. By understanding the basic principles of supply and demand, as well as the key terms and concepts involved, individuals can gain a deeper appreciation for how the economy works and make more informed decisions.